Yesterday, the California Association of Realtors (C.A.R.) released their third quarter housing numbers.

The data presented this quarter might be some of the most important received in all of 2020. For this blog, I want to highlight a few facts from the C.A.R. report. Then, I want to dig deeper into housing affordability numbers and how it might affect the market over an extended period of time.

C.A.R’s 3rd Quarter Report & Affordability

The title of C.A.R.’s press release was: “Higher Home Prices Driven by Dearth of Inventory Depresses California Housing Affordability in Third-Quarter 2020.”

Some of their main bullet points were the following:

- Just 28% of California households could afford to buy the $693,680 median-priced home in Q3 of 2020. That is an incredibly significant drop from the 33% seen just last quarter.

- The minimum annual income needed to make payments on that median-priced home with 20% down is $127,200. Those monthly payments are estimated at about $3,180 per month assuming principal, interest, and taxes are at a 30-year fixed rate of 3.15%.

- More Californians can afford the median-priced condo or town home. At a $512,000 median price, 42% of the buyers can purchase those asset types with an annual income of $94,000.

As stated in their press release, C.A.R. believes that their Housing Affordability Index is the most fundamental measure of housing well-being for home buyers in the state.

And, I couldn’t agree more.

Housing affordability is fast becoming the most important issue affecting our local market and the state.

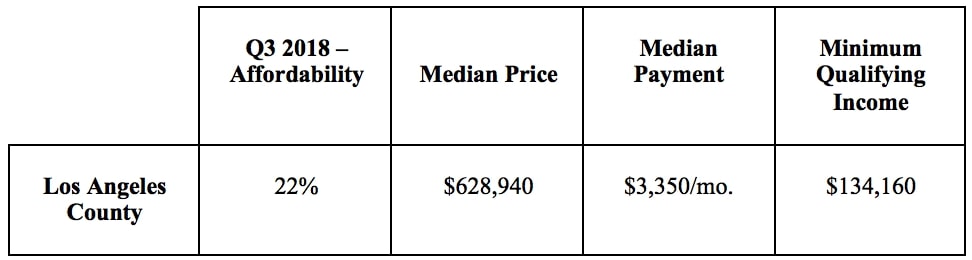

The county of Los Angeles is even less affordable than the state with only 23% of home buyers able to afford the median-priced home. Currently, a home’s median price in the county sits at $708,870.

The statewide median price in Q3 increased 13.6% from the previous quarter and by almost the same amount year-over-year. Price growth like that is unbelievable and a huge factor for why affordability has plummeted, even with historically low interest rates.

I believe price growth, all-time low interest rates, and dropping affordability are all major factors in dictating how this market performs in the future. Everyone should follow these numbers closely to make good decisions with regards to their real estate acquisitions and dispositions.

Affordability & Interest Rates

As mentioned in past blogs, I believe that median income and affordability needs to be discussed more often, and, thoroughly. This can be the key to rising or falling real estate prices.

In a blog almost two years ago, I looked at 2018 Q3 affordability numbers and tried to break down the median income of South Bay markets in comparison to their median prices.

That blog is timely for comparison to present day and is worth a re-read. To re-visit that blog for a refresher, click here.

I will do this same analysis for 2020 in a future blog, but for now, I want to focus on our local county’s price, along with interest rates and affordability.

Check out L.A. County 2018 Q3 Affordability numbers from the old blog:

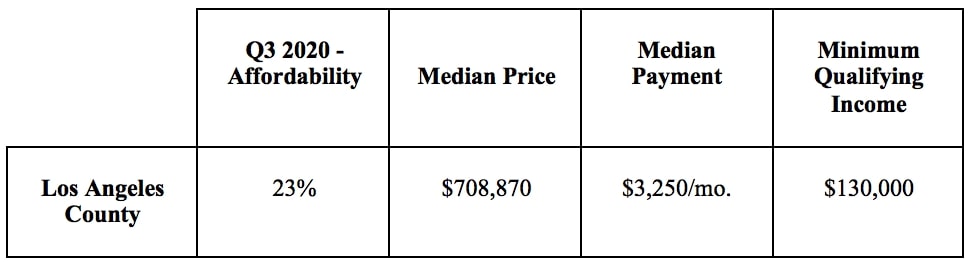

Now, check out L.A. County 2020 Q3 Affordability numbers that were just released:

With the exception of price, which is $80,000 higher today, all the numbers are essentially the same! What gives?

Ultra-low interest rates helping to off-set the rise in price.

You also have to love how efficient and dynamic our market is. When interest rates plummeted, affordability went way up, and buyers went in and gobbled everything up until affordability went back down again.

In Q3 of 2018, interest rates were around 4.7%.

In Q3 of 2020, interest rates were around 2.9%…or 3.15% according to C.AR.

Interest rates reached a peak at almost 5% at the end of 2018 and steadily began dropping, allowing for homes to become more affordable and keep the market going higher.

In Q3 and Q4 of 2019, affordability was at 25% and 27% respectively.

When The Fed slashed interested rates lower, Q1 and Q2 of this year saw affordability jump to 31% and 32% respectively.

In just a quarter, buyers have taken advantage of that affordability thanks to all-time low interest rates and swarmed the market. The market is so efficient that in just two quarters, the extra affordability has been completely wiped out.

Even with all-time low interest rates, it is no longer a benefit, as owning a home now is just as expensive as owning one back in 2018.

And, that is the key point…all-time low interest rates are now no longer a reason to own a home.

Think about that.

The market has officially rebalanced, where prices are meaningfully higher thanks to low interest rates. It will cost you the same overhead as it did in 2018, and, you need to come up with a larger down payment.

Interest rates have been the driving force in this amazing price surge. COVID-19 may have a little something to do with it too…

Using Median Income to Predict Price

Bruce Norris has been made famous by using affordability numbers to predict price tops and bottoms.

I have studied his work and, in general, California has hit peak pricing when affordability hits 17%. Thanks to liar loans that fueled the Great Recession and housing crisis, California reached peak price when affordability reached levels at 13%.

Bruce has stated that with tighter loan standards, we likely will not see 17%, but a slightly higher affordability number as a peak in price.

In 2018, Bruce released charts for major counties that considered how high prices could run depending on prices and interest rates. I want to re-share that chart since interest rates have changed dramatically over two years.

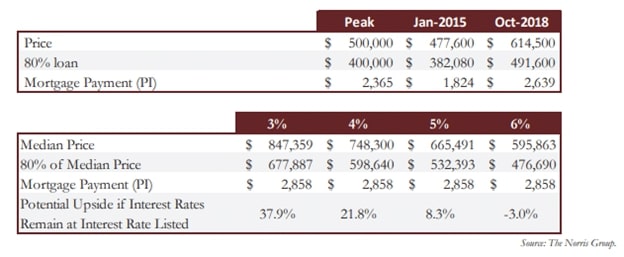

This is Norris’ L.A. County chart back in 2018:

As you can see, Norris’ chart calculates that Los Angeles County can support an $847,359 price at 3% interest rates. We currently sit at a price of $708,870 for the third quarter.

The numbers get even tighter when considering the month of September. According to C.A.R., the county of Los Angeles sits at a median price of $747,380 for September of 2020.

So, if rates stay the same, do we have another $100,000 or 13% growth in the local housing market?

Furthermore, what if we see rates go back to 4%…does that mean the market will have gone as high as it can go?

Conclusion

Goldman Sachs released a note today about The Fed’s commitment to not raise rates until inflation is consistently above 2%. In Goldman’s view, they see no rate increases until early 2025.

So, if you are believer in 30-year mortgage rates holding strong at 3%, then this market still has room for continued strength.

If you believe inflation comes and rates need to rise sooner, then rising rates might be the greatest threat to this real estate market and induce price weakness if we approach 4% rates.

It is impossible to predict price movements…and interest rates for that matter.

But, when you take median income, median prices, and interest rates, and then compare them to historical housing affordability numbers during boom and bust cycles, you have a pretty powerful mathematical tool to make educated guesses on how to manage your real estate investment dollars.

Richard Haynes

DRE: 01779425

For more South Bay real estate insights, subscribe and follow Richard’s social channels below:

A leader in South Bay real estate for the better part of a decade, Richard thrives as an advisor to his clients with over $248 million in sales as a broker or investment principal at his boutique agency, Haynes. Richard is known for his keen local market insights which have been featured in the L.A. Times, The Street, and Forbes, along with his weekly South Bay real estate blog. [read more]